|

||||||||

| March 1, 2017 | ||||||||

| PowerFloat Plus nozzles cut energy by almost 20% at Ishinomaki |  |

|||||||

|

· Subscribe to Ahead of the Curve · Newsletters · Ahead of the Curve archived issues · Contact the Editor

|

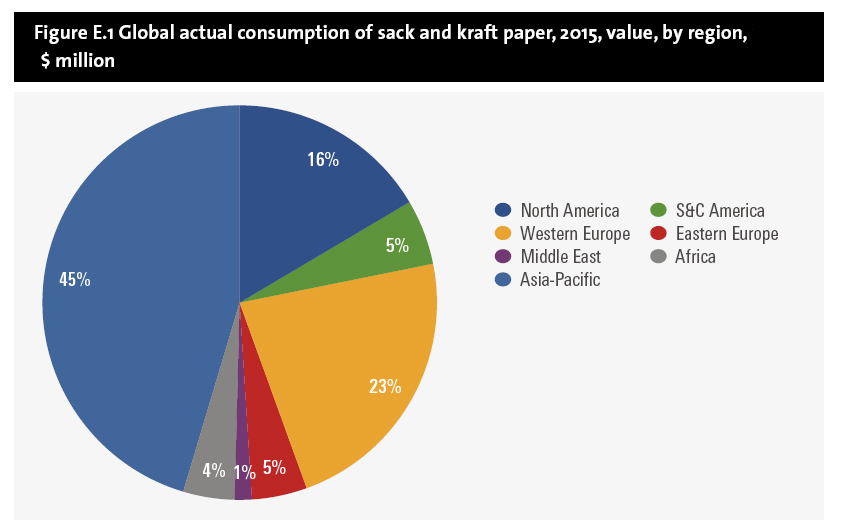

Sack and kraft packaging demand is shifting to consumer application JOHN NELSON World demand for sack and kraft paper used in packaging is set for healthy annual growth of three percent across the next five years, according to the latest exclusive research from Smithers Pira. In 2016, demand from this segment stood at over 23 million metric tons of material and held a value worldwide of US$66 billion, according to the new market study The Future of Sack and Kraft Paper to 2021. Its analysis charts how the market will expand to reach almost 28 million metric tons by 2021, valued at about US$80 billion at 2016 prices. This expansion is taking part against a backdrop of changes within the sack and kraft industry, placing a premium on technical innovation. The most important influence on consumption of these materials remains in the hands of the end user. Shifts in buying patterns among consumers impact on all end-use applications and ultimately drive the demand for all packaging. Consumption in traditional industrial applications is being eroded as sack formats are displaced by plastic and metal bulk and semi-bulk handling containers. This is being countered by increasing enthusiasm from consumer segments. Consumer priorities This is placing pressure on papermakers to develop innovative solutions to provide suitable and appropriate printing surfaces. A particular priority is to evolve solutions that can interface with digital—inkjet and toner—print technologies that enable short and customised editions of packaging creating value-adding opportunities for converters.

Another key development addressing this shift has been the introduction of ultrasonic sealing machinery. This technology can simultaneously offer a tighter closure and ejects loose material from the region of the valve seal, which enables faster and smoother filling processes that can translate into marked reductions in costs for converters. Sustainability This impetus is also leading paper producers to bolster the environmental credentials of their sack and kraft grades. Adoption of sustainability practices has been fairly widespread throughout much of the industry and many suppliers now sport a plethora of environmental certifications – such as those approved by the Forest Stewardship Council (FSC). As environmental pressures become ever greater, it is possible that kraft and sack paper manufacturers may start to develop entire product ranges marketed on a sustainability platform. In addition to sourcing from sustainably managed forests, some kraft paper producers have also made attempts to increase the amount of recycled material used in the manufacture of their products. Across 2016-2021, sustainability certification is expected to become ever more widespread, with penetration of eco-labels increasing in parts of the world where their presence has been limited to date. Downgauging This trend naturally cuts the weight of paper demanded, but demographic shifts in consumer markets are again helping to mitigate this. There is a wider trend in packaging towards smaller pack sizes as typical family units get smaller, since smaller sizes boost convenience and reduce food wastage for the end user. This is having a positive impact on the industry as one 500g pack consists of less material than two 250g packs, and there is a corresponding demand for more consumables, such as inks and adhesives that build the bag. North American outlook In North America, sugar and flour account for over a quarter of the demand for sack and kraft packaging papers, with the other major dry goods markets adding a further 20 percent of the total. Industrial applications represent just over 41 percent of total demand in 2015, though this will decline across the next five years for the reasons outlined above. M&A Consolidation among both raw material suppliers and converters is slowly changing the dynamics of the market. Mergers like that of MeadWestvaco and RockTenn to create WestRock in 2015, is encouraging other suppliers to consolidate further to redress the competitive balance. Further consolidations at end-user level will also have an indirect impact on this market as newly formed user companies assert their increased buying power by switching packaging suppliers into one source, thus eroding the client base of the losing supplier.

The full impact of these market and technology drivers in different regions across the world is analyzed and quantified in depth in Smithers Pira’s report The Future of Sack and Kraft Paper to 2021. John Nelson is commissioning editor, Smithers Pira. Smithers Pira is a global authority on the packaging, paper, and print industry supply chains. Smithers publishes market intelligence, product testing, and can provide a range of custom consultancy services for firms operating in these markets.

For a modest investment of $174, receive more than US$ 1000 in benefits in return. |

|||||||

|

||||||||