| |

· www.tappi.org

· www.tappi.org

· Subscribe

to Ahead of the Curve

· Newsletters

· Ahead

of the Curve archived issues

· Contact

the Editor

|

|

|

|

The European Containerboard Market

UNBAN LUNDBERG

Editor's note: The following article appears in the July/August issue of Paper360° magazine, and is offered here to Ahead of the Curve readers who may have missed it.

The European containerboard market is currently experiencing a "golden time." Strong demand, high prices, low OCC costs, and stable profits make it easy to be optimistic. But factors that could impact the sector's ability to sustain this growth must also be considered if it is to remain strong.

Current Capacity Growth and 'Red Flags'

Market demand for containerboard is still quite strong, and has led to investments in capacity growth, primarily in the top-quality tiers of testliner. But capacity growth is also coming from producers in other grades, primarily printing & writing and newsprint, as many are converting their machines as a result of declining demand.

However, these companies are not concerned with the impact of building up containerboard overcapacities. This could prove to be problematic as opportunities to replace imported kraftliner are limited due to quality requirements and price. Additionally, European exports are unlikely to increase dramatically due to its uncompetitive cost position. This is creating increasing pressure for smaller, less efficient European plants to shut down.

Capacity Growth Trends

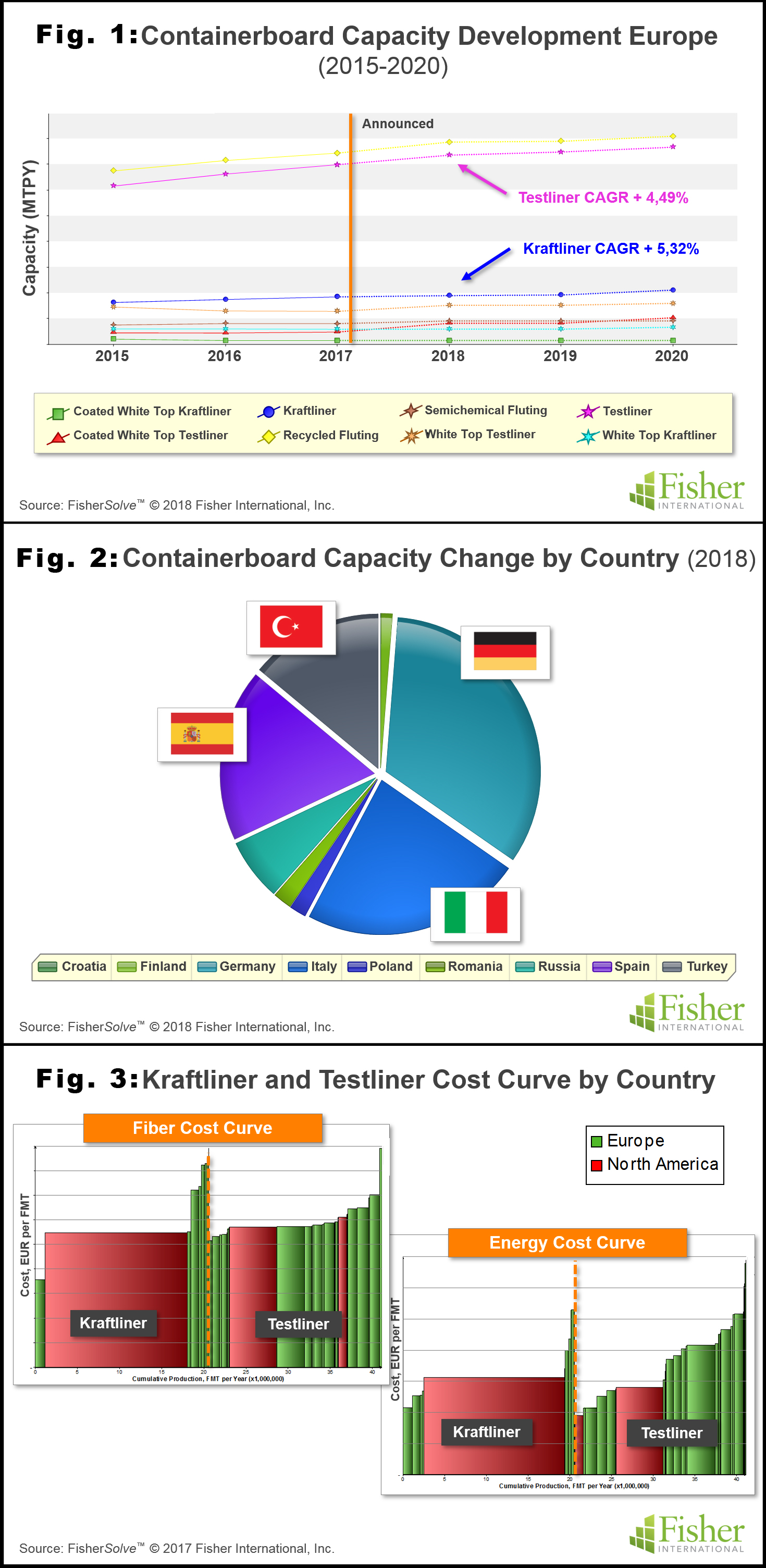

As shown in Figure 1, an analysis of containerboard capacity development in Europe looks healthy, with an average forecasted CAGR of about 5 percent.

When looked at from a global perspective (excluding China), Europe currently accounts for 50 percent of the announced capacity growth for containerboard, with recycled containerboard representing 90 percent of the announced capacity growth in 2018. Almost half of this capacity growth is driven by rebuilt machines, by virtue of the fact that they offer a lower investment option than new or secondhand machines. Interestingly, most of the added European capacity is located in Germany, Italy, Spain and Turkey (Fig. 2).

Testliner comprises about half of the European containerboard market, with kraftliner taking a very small portion. In North America, these values are reversed and kraftliner is much bigger than testliner. The primary reason for this is Europe's large dependency on recycled rather than virgin fiber.

Will the Good Times Last?

Longevity and sustainability of containerboard growth in Europe depends upon four key factors: demand, US exports of kraftliner, new capacity due to pressure from declining grades to convert, and the number of small machine mills that will close.

Currently, containerboard demand is increasing due to an overall strong economy and e-commerce. Eventually, however, packaging costs will become an issue and producers must be prepared to meet pressures/new regulations surrounding packaging redesign. How swiftly the industry players adapt will determine which ones succeed and which will fail. Unknown variables such as increases in global trade disputes could also impact demand.

US exports have been relatively stable over the past five years, but changes in market conditions could drive exports higher. Europe's shortage of kraftliner, for example, may be unable to meet growing demand and could provide inroads for additional US exports, since even top quality testliner is not always substitutable. Europe is also at a significant cost disadvantage, mainly due to high fiber and energy costs (Fig. 3). Lastly, kraftliner conversion opportunities appear to be stronger in North America, which would make more product available for export.

Restructuring is Inevitable

An analysis of the European containerboard industry reveals it is highly fragmented, with dozens of small corporations, nearly two-thirds of them being private. Conversely, in North America, containerboard production is highly consolidated and in primarily public-based companies. The ability for any one company in Europe to have a dominant market share will require multiple mergers. The timeline for mergers becomes longer and more challenging when the impact of private ownership is considered.

These issues could provide opportunities for American companies to grow through acquisition in Europe, especially given the fact that the US market is already quite consolidated, with limited capacity for growth. China could also become a major player in the European consolidation, shifting its focus from pulp to other profit-generating opportunities.

Conclusions

While focusing on paper production assets is critical to producers, companies that stand the best chance for sustainable success are those that consider the entire value chain: the paper production, the corrugators, and a solid go-to-market organization with a strong end-customer relationships.

Viability benchmarking is an ideal way to identify the mills or machines at risk across a number of factors including cost, size, capital requirements, tons per inch trim, technical age, location, and internal company risk, and is an exercise that should be considered.

By virtue of its deep expertise in the pulp and paper industry, Fisher International can provide insights, intelligence, benchmarking, and modeling across myriad scenarios. This knowledge can help companies gain a better understanding of their strengths and identify weaknesses, which helps them stave off challenges and better position themselves for long-term growth.

About the author:

Unban Lundberg is senior consultant, Fisher International, Inc., which supports the pulp and paper industry with business intelligence and strategy consulting. For more information visit www.fisheri.com.

For a modest investment of $174, receive more than US$ 1000 in benefits in return.

Visit www.tappi.org/join for more details. |

|