Global Development and M&A Investment in the Paper Industry

Global Development and M&A Investment in the Paper Industry

This article will appear in the upcoming May/June issue of Paper360° magazine. It is being shared here as a special "sneak peek" for Ahead of the Curve readers. The global pulp and paper industry is entering a new phase of structural transformation. While overall growth remains steady, regional divergence is becoming more pronounced, product demand is shifting, and trade and regulatory pressures are reshaping traditional expansion paths. At the same time, mergers and acquisitions are increasingly serving as a strategic tool for companies seeking scale, resilience, and access to new markets.

This article examines key global development trends in the pulp and paper industry from 2009 through 2028, highlights the changing role of emerging economies, and explores how investment and M&A strategies—particularly among Chinese producers—are evolving in response to these dynamics.

Global Development Trends

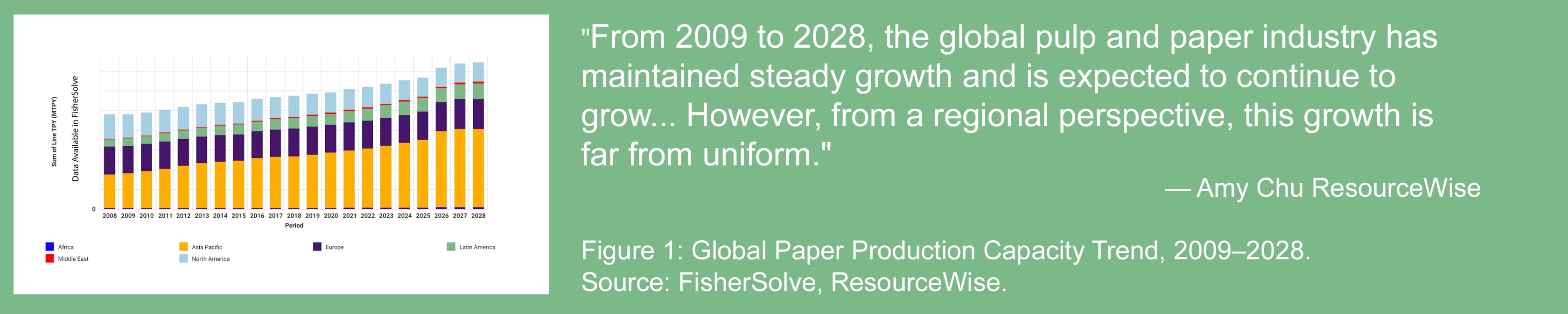

From 2009 to 2028, the global pulp and paper industry has maintained steady growth and is expected to continue to grow at a compound annual growth rate (CAGR) of 2.3 percent.

However, from a regional perspective, this growth is far from uniform. Significant differences exist in both capacity scale and growth rates across regions (Fig. 1).

Asia-Pacific is the fastest-growing region globally. By 2028, capacity is expected to grow exponentially since 2009 levels. While growth is projected to moderate between 2025 and 2028 due to a slowdown in new investments, the region will continue to lead global expansion.

Latin America follows closely behind, with capacity expanding by around 100 percent from 2009 to 2025. The growth, especially recent growth, is driven primarily by large-scale pulp projects in Brazil, Argentina, and other countries. Although the Middle East has a relatively small capacity base, expansion led by equipment suppliers and service providers has driven a high CAGR of 8.0 percent, positioning the region as a new growth pole for the industry.

In contrast, North America and Europe are experiencing relatively stable growth. In these mature markets, the industry focus is shifting from “capacity expansion” toward “efficiency optimization.” The core reason for this regional imbalance lies in the rising demand for packaging and tissue driven by industrialization and urbanization in emerging economies, while developed markets are increasingly saturated and constrained by stricter environmental regulations governing new capacity.

BRICS as Main Driver of Capacity Growth

Emerging economies, represented by the BRICS countries, continue to increase their share of global paper capacity and have become the industry's core growth engine. In 2009, BRICS countries (excluding new members such as Indonesia and Iran, added in 2025) accounted for only 24 percent of global pulp capacity. By 2028, the BRICS share is expected to exceed 50 percent, with China, Brazil, and India remaining the primary contributors to global capacity growth.

China: Continued Growth, Surge in Exports

China remains the world’s largest paper-producing country. From 2022 to 2025, the industry recorded a CAGR of over seven percent, with particularly strong growth in folding boxboard and printing and writing grades. However, over the past two years, the number of new projects has declined sharply. Several projects announced in 2025 have been delayed or canceled, and industry-wide CAGR is expected to fall over the next year.

From a grade perspective, containerboard still has some growth potential, while market pulp expansion is increasingly concentrated in specialty pulp. Notable examples include specialty pulp projects developed by Huatai and Yunjing. Tissue continues to show steady growth, with new capacity announcements in 2026 to 2027.

The decline in new paper machine installations in China reflects the broader slowdown. New paper machines peaked at around 150 units in 2022, declined to 120 units in 2025, and are expected to fall further by 2027. This trajectory mirrors that of developed markets such as the United States and Germany, which reached peak capacity in the 1950s–1960s and subsequently entered a phase of “stock competition.”

In recent years, China’s exports of paper and paperboard have grown rapidly. In 2024, exports reached approximately nine million tons, accounting for nearly ten percent of global paper and paperboard trade. China surpassed the US to become the world’s second-largest exporter, behind Germany.

This rapid expansion has triggered increasingly aggressive trade countermeasures from major trading partners. The US imposed tariffs of 62.07-73.5 percent on Chinese paper shopping bags in July 2024 and a 267.63 percent tariff on paper plates in January, 2025. The EU imposed tariffs of 26.4-26.6 percent on Chinese decorative paper plates in August, 2025.

India imposed tariffs of US$152.27-221.36 per ton of FBB/SBS/LPB in September, 2025, despite China exporting only 170-200 thousand tons annually to India. Mexico, Brazil, Pakistan, and others have also launched anti-dumping and countervailing investigations, further intensifying trade friction.

Inevitable Path for Industry Development

In recent years, M&A activity in the global paper industry has remained robust, evolving from simple capacity consolidation to broader upstream and downstream integration. Several landmark transactions emerged in 2025:

- January: International Paper merged with DS Smith, creating a joint packaging paper company.

- March: India’s largest paper producer, ITC, acquired Century Pulp and Paper.

- June: PCA acquired two paper mills and eight packaging plants from Greif.

- July: Oji Holdings acquired AustroCel Hallein, extending upstream into pulp production.

Western paper companies focus on “geographic complementarity,” “scale coordination,” and “efficiency improvement,” often optimizing portfolios by shutting down inefficient capacity. However, their global influence is gradually declining, while Asian—especially Chinese—companies continue to expand capacity and gain market share.

Key M&A Strategies of Chinese Companies

Facing escalating trade barriers, tightening raw material constraints, and intensifying competition, Chinese paper companies have developed five major M&A strategies:

- Localized production to offset trade barriers.

- Forest-pulp-paper integration to secure cost and compliance advantages.

- Overseas recycling fiber processing to address domestic supply constraints.

- Deepening investment in Belt and Road and ASEAN markets.

- Technology-driven and product-portfolio acquisitions and upgrades.

Specialty Paper: A Segment to Watch

As overcapacity intensifies in traditional paper grades, Chinese producers are increasingly shifting their focus toward specialty paper. In 2025, China accounted for about 30 percent of total specialty papers capacity. China has transitioned from a net importer in 2009 to a net exporter in 2025, with approximately six percent of domestic capacity requiring export markets.

The global specialty paper sector remains highly fragmented. While Chinese companies can often surpass overseas peers in scale, identifying suitable acquisition targets that align with corporate culture and generate long-term value remains a critical challenge.

Navigating Change in a Transforming Industry

As the global pulp and paper industry becomes more regionally diverse, trade-constrained, and strategically complex, data-driven investment decisions and well-executed M&A strategies are increasingly essential. Companies expanding overseas must navigate regulatory risk, supply chain integration, and market positioning with precision.

Amy Chu is a senior consultant at ResourceWise. ResourceWise provides data, analytics, and consulting services for a robust range of natural-resource-based commodity industries, including forest products, low-carbon feedstocks and fuels, and chemicals. Visit resourcewise.com.

This article examines key global development trends in the pulp and paper industry from 2009 through 2028, highlights the changing role of emerging economies, and explores how investment and M&A strategies—particularly among Chinese producers—are evolving in response to these dynamics.

Global Development Trends

From 2009 to 2028, the global pulp and paper industry has maintained steady growth and is expected to continue to grow at a compound annual growth rate (CAGR) of 2.3 percent.

However, from a regional perspective, this growth is far from uniform. Significant differences exist in both capacity scale and growth rates across regions (Fig. 1).

Asia-Pacific is the fastest-growing region globally. By 2028, capacity is expected to grow exponentially since 2009 levels. While growth is projected to moderate between 2025 and 2028 due to a slowdown in new investments, the region will continue to lead global expansion.

Latin America follows closely behind, with capacity expanding by around 100 percent from 2009 to 2025. The growth, especially recent growth, is driven primarily by large-scale pulp projects in Brazil, Argentina, and other countries. Although the Middle East has a relatively small capacity base, expansion led by equipment suppliers and service providers has driven a high CAGR of 8.0 percent, positioning the region as a new growth pole for the industry.

In contrast, North America and Europe are experiencing relatively stable growth. In these mature markets, the industry focus is shifting from “capacity expansion” toward “efficiency optimization.” The core reason for this regional imbalance lies in the rising demand for packaging and tissue driven by industrialization and urbanization in emerging economies, while developed markets are increasingly saturated and constrained by stricter environmental regulations governing new capacity.

BRICS as Main Driver of Capacity Growth

Emerging economies, represented by the BRICS countries, continue to increase their share of global paper capacity and have become the industry's core growth engine. In 2009, BRICS countries (excluding new members such as Indonesia and Iran, added in 2025) accounted for only 24 percent of global pulp capacity. By 2028, the BRICS share is expected to exceed 50 percent, with China, Brazil, and India remaining the primary contributors to global capacity growth.

China: Continued Growth, Surge in Exports

China remains the world’s largest paper-producing country. From 2022 to 2025, the industry recorded a CAGR of over seven percent, with particularly strong growth in folding boxboard and printing and writing grades. However, over the past two years, the number of new projects has declined sharply. Several projects announced in 2025 have been delayed or canceled, and industry-wide CAGR is expected to fall over the next year.

From a grade perspective, containerboard still has some growth potential, while market pulp expansion is increasingly concentrated in specialty pulp. Notable examples include specialty pulp projects developed by Huatai and Yunjing. Tissue continues to show steady growth, with new capacity announcements in 2026 to 2027.

The decline in new paper machine installations in China reflects the broader slowdown. New paper machines peaked at around 150 units in 2022, declined to 120 units in 2025, and are expected to fall further by 2027. This trajectory mirrors that of developed markets such as the United States and Germany, which reached peak capacity in the 1950s–1960s and subsequently entered a phase of “stock competition.”

In recent years, China’s exports of paper and paperboard have grown rapidly. In 2024, exports reached approximately nine million tons, accounting for nearly ten percent of global paper and paperboard trade. China surpassed the US to become the world’s second-largest exporter, behind Germany.

This rapid expansion has triggered increasingly aggressive trade countermeasures from major trading partners. The US imposed tariffs of 62.07-73.5 percent on Chinese paper shopping bags in July 2024 and a 267.63 percent tariff on paper plates in January, 2025. The EU imposed tariffs of 26.4-26.6 percent on Chinese decorative paper plates in August, 2025.

India imposed tariffs of US$152.27-221.36 per ton of FBB/SBS/LPB in September, 2025, despite China exporting only 170-200 thousand tons annually to India. Mexico, Brazil, Pakistan, and others have also launched anti-dumping and countervailing investigations, further intensifying trade friction.

Inevitable Path for Industry Development

In recent years, M&A activity in the global paper industry has remained robust, evolving from simple capacity consolidation to broader upstream and downstream integration. Several landmark transactions emerged in 2025:

- January: International Paper merged with DS Smith, creating a joint packaging paper company.

- March: India’s largest paper producer, ITC, acquired Century Pulp and Paper.

- June: PCA acquired two paper mills and eight packaging plants from Greif.

- July: Oji Holdings acquired AustroCel Hallein, extending upstream into pulp production.

Western paper companies focus on “geographic complementarity,” “scale coordination,” and “efficiency improvement,” often optimizing portfolios by shutting down inefficient capacity. However, their global influence is gradually declining, while Asian—especially Chinese—companies continue to expand capacity and gain market share.

Key M&A Strategies of Chinese Companies

Facing escalating trade barriers, tightening raw material constraints, and intensifying competition, Chinese paper companies have developed five major M&A strategies:

- Localized production to offset trade barriers.

- Forest-pulp-paper integration to secure cost and compliance advantages.

- Overseas recycling fiber processing to address domestic supply constraints.

- Deepening investment in Belt and Road and ASEAN markets.

- Technology-driven and product-portfolio acquisitions and upgrades.

Specialty Paper: A Segment to Watch

As overcapacity intensifies in traditional paper grades, Chinese producers are increasingly shifting their focus toward specialty paper. In 2025, China accounted for about 30 percent of total specialty papers capacity. China has transitioned from a net importer in 2009 to a net exporter in 2025, with approximately six percent of domestic capacity requiring export markets.

The global specialty paper sector remains highly fragmented. While Chinese companies can often surpass overseas peers in scale, identifying suitable acquisition targets that align with corporate culture and generate long-term value remains a critical challenge.

Navigating Change in a Transforming Industry

As the global pulp and paper industry becomes more regionally diverse, trade-constrained, and strategically complex, data-driven investment decisions and well-executed M&A strategies are increasingly essential. Companies expanding overseas must navigate regulatory risk, supply chain integration, and market positioning with precision.

Amy Chu is a senior consultant at ResourceWise. ResourceWise provides data, analytics, and consulting services for a robust range of natural-resource-based commodity industries, including forest products, low-carbon feedstocks and fuels, and chemicals. Visit resourcewise.com.

Inside this Section

-

- Arthur J. Ragauskas, Ph.D., Rises to Role of TAPPI Journal Editor-in Chief

- Advanced Coating Symposium 2026 Call for Speakers Now Open

- New President and CEO Annoucement

- TAPPI Announces Call for Speakers for TAPPICon 2026

- TAPPI Announces Important Changes to Its Nano Division

- TAPPI’s Paper and Board Division Announces Formation of a Fiber Molding Committee

- Keynote Speakers Announced for TAPPI Nano 2025 in Girona, Spain

- TAPPI Journal Awards Best Research Paper for 2024

- TAPPI Selects Fellows and Outstanding Young Professional for 2025

- Group Chief Executive Officer and President of Smurfit Westrock Receives TAPPI/PIMA 2025 Executive of the Year Award

- David Schwerbel, Principal of Telos-US, Named Recipient of TAPPI’s Paul W. Magnabosco Outstanding Local Section Award

- Anthony “Tony” Lyons, Ph.D., Honored with TAPPI’s 2025 Herman L. Joachim Distinguished Service Award

- Wadood Y. Hamad, Ph.D., Named Recipient of TAPPI’s 2025 Gunnar Nicholson Gold Medal Award

- TAPPICon 2025 Expands to Include Pulp and Fiber Innovation

- Important Leadership Changes in 2025

- TAPPI Journal Announces New Editorial Board Members

- Subject Matter Experts Invited to Present at TAPPICon 2025

- Early Bird Registration Opens for Two Co-Located TAPPI Courses

- TAPPI/AICC’s 2024 Box Manufacturing Olympics Winners Announced

- TAPPI’s Corrugated Packaging Council Elects Two New Members

- SuperCorrExpo 2024 comes to a close, exceeding expectations

- Fiberglass Mat Community to Meet October 1-3, 2024 in Denver, CO

- TAPPI/AICC Announce Cris Carter to Keynote at SuperCorrExpo® 2024

- TAPPI & AICC Now Accepting Entries for Box Manufacturing Olympics

- TAPPI & AICC Announce Attendee Registration Opening for SuperCorrExpo® 2024

- Sean Ireland, CEO of CapaTec, to Deliver Keynote Address at TAPPI's 2024 International Conference on Nanotechnology for Renewable Materials (Nano)

- Sean Ireland, CEO of CapaTec, to Deliver Keynote Address at 2024Nano

- CEO of ND Paper Receives TAPPI/PIMA 2024 Executive of the Year Award

- TAPPI Selects Fellows and Outstanding Young Professionals for 2024

- Converter Advanced Registration Discount (CARD) Program Provides Affordable, One Price Registration

- Paula Hajakian Honored with TAPPI’s 2024 Herman L. Joachim Distinguished Service Award

- Seyhan Nuyan, Ph.D., Named Recipient of TAPPI’s 2024 Gunnar Nicholson Gold Medal Award

- What’s In Your Flexible Packaging?

- TAPPI Announces Newly Elected Directors from Irving Consumer Products, Valmet and Auburn University

- TAPPI Journal Awards Best Research Paper for 2023 and Announces Editorial Board Changes for 2024

- Early-bird Registration Opens for the 2024 TAPPI International Conference on Nanotechnology for Renewable Materials

- TAPPI/AICC Announce Jake Hall and Greg Gumbel to Keynote at SuperCorrExpo

- Corrugated Boot Camp Hosted by Chicago TAPPI Following Annual Board Meeting

- TAPPI Foundation Names 2023-2024 Scholarship Winners

- Call for Presentations Extended for TAPPI’s FlexPack PLACE Conference

- Fiberglass Mat Community to Meet October 17-19, 2023 in Chattanooga, TN

- Abstracts Sought for TAPPI’s FlexPack PLACE Conference

- TAPPI Announces CorrExpo 2023 What’s New/Tech Talks Presentations

- TAPPI Announces 2023 Award Winners For the Corrugated Packaging Division

- Announcing TAPPI’s CorrExpo 2023 Box Plant Deal

- TAPPI’s Women in Industry Division Names Sappi North America’s Vice President of Research, Development and Sustainability and North Carolina State University’s Assistant Dean for Advancement in the College of Natural Resources Recipients of the 2023 Woman

- Announcing TAPPI’s CorrExpo 2023 Keynoters: Bob Chapman, Chairman and CEO, Barry-Wehmiller and World-Class Drummer Mark Schulman

- President and CEO of Stora Enso Receives TAPPI/PIMA 2023 Executive of the Year Award

- TAPPI Journal Awards Best Research Papers for 2022

- TAPPI Selects Fellows and Outstanding Young Professionals for 2023

- Brian N. Brogdon Honored with TAPPI’s 2023 Herman L. Joachim Distinguished Service Award

- North Carolina State University’s Professor and Buckman Distinguished Scientist Named Recipient of TAPPI’s 2023 Gunnar Nicholson Gold Medal Award

- TAPPI Announces New Directors and Officers of the Board

- TAPPI Journal Announces New Editorial Board Members

- Chemical Recovery in the Alkaline Pulping Processes, Fourth Edition Now Available from TAPPI Press

- Education and Networking to Take Center Stage at Fiberglass Mat Event

- Innovation to Take Center Stage at Biennial European PLACE Conference

- New Handbook Assists Paper Mills to Achieve Efficient Operation through Utilization of Process Chemicals

- Chairman and CEO of Green Bay Packaging Inc. Receives TAPPI/PIMA 2022 Executive of the Year Award

- TAPPI Journal Awards Best Research Paper for 2021

- TAPPI Selects Fellows and Outstanding Young Professionals for 2022

- Paul W. Magnabosco Outstanding Local Section Award

- John Neun Named Recipient of 2022 Herman L. Joachim Distinguished Service Award

- WestRock’s Director-Research and Innovation Named Recipient of TAPPI’s 2022 Gunnar Nicholson Gold Medal Award

- Introducing TAPPI’s Newest Directors

- Interactive Panel Provides Perspectives on 2025 Sustainability Initiatives In the Flexible Packaging Industry

- Two Major Training Events for the Pulp and Paper Industry Set for January 10 – 13, 2022 in St. Petersburg, Florida

- TAPPI Foundation Awards 2021-2022 Scholarships

- Lime Kilns and Recausticizing: The Forgotten Part of a Kraft Mill Now Available from TAPPI Press

- TAPPI Journal Awards Two Best Research Papers for 2020

- New TAPPI Board of Directors and Officers Announced

- TAPPI Announces 2020 Engineering Division Technical Award and Beloit Prize Winner

- TAPPI Academy Announces Addition of Web and Winding Courses to eLearning Offerings

- TAPPI Announces Cash Prize to Accompany TAPPI Journal Best Research Paper Award

- Master Papermaking Additives to Gain Competitive Advantage and Better Meet Customers’ Needs

- Film Extrusion Manual, Third Edition Now Available from TAPPI Press

- TAPPI Selects Fellows and Outstanding Young Professionals for 2020

- Black Liquor Evaporation Now Available from TAPPI Press

- Kraft Recovery Boilers, Third Edition Now Available From TAPPI Press

-

- April 2019 Committee of the Month - Runnability Planning Committee

- Mentor Match Signup - Spring 2019

- A Guide to the Nanotechnology used in the Average Home

- 65 North American Companies Remove Go Paperless - Go Green Claims

- 5,000 journals articles and conference papers now available to search

- 2017 starts with sales soaring for paper diaries, notebooks and planners

- 20 never seen before packaging designs

- Better Together Podcast

-

- My TAPPI Story: Naomi Gehling

- My TAPPI Story: Leslie Petrie

- My TAPPI Story: David Maddux

- My TAPPI Story: Eupidio Scopel

- My TAPPI Story: Prakash Malla

- My TAPPI Story: Doug Coffin

- My TAPPI Story: Rory Wolf

- My TAPPI Story: Peter Hart

- My TAPPI Story: Greg Jones

- My TAPPI Story: Gabriele Pinckney

- My TAPPI Story: Jimmy Jong

- My TAPPI Story: Mike Farrell